Lately the founders have been facing questions about the emission schedule. Instead of responding to these questions individually, we find it more appropriate to post a public response: The emission schedule will not be changed by any of the founders, nor will any such change be endorsed by a founder in the future.

The blockchain is not merely “internet money” as the legacy financial sector is perfectly capable of creating great apps that allow for the easy transfer of digitized money. Nor is the blockchain merely a casino that allow people to gamble on the latest fad in the hopes of earning 10.000 % on their investment. The legacy financial sector is also capable of delivering that. As we see it, the blockchain is first and foremost a rebellion against arbitrary power over money. It exists to give people, if not certainty of the value of their coins in the future, then at least certainty of the rules and future amounts of those coins. If such a rebellion is to be successful, we cannot allow for the replacement of one privileged class over another; we cannot give ourselves the power that we wish to take away from other. Setting the precedence that the emission schedule is up for debate gives maintainers and stakeholders the power that no one must have. Furthermore, it jeopardizes one of the most appealing features of (good) blockchains: the inelasticity of the money supply. If the price of gold rises, gold resources that were previously uneconomical to extract might become valuable enough that they can be extracted profitably, leading the available supply of gold to rise when the price rises. Better money than gold does not have this deficiency, its supply is unaffected by the demand, in either direction.

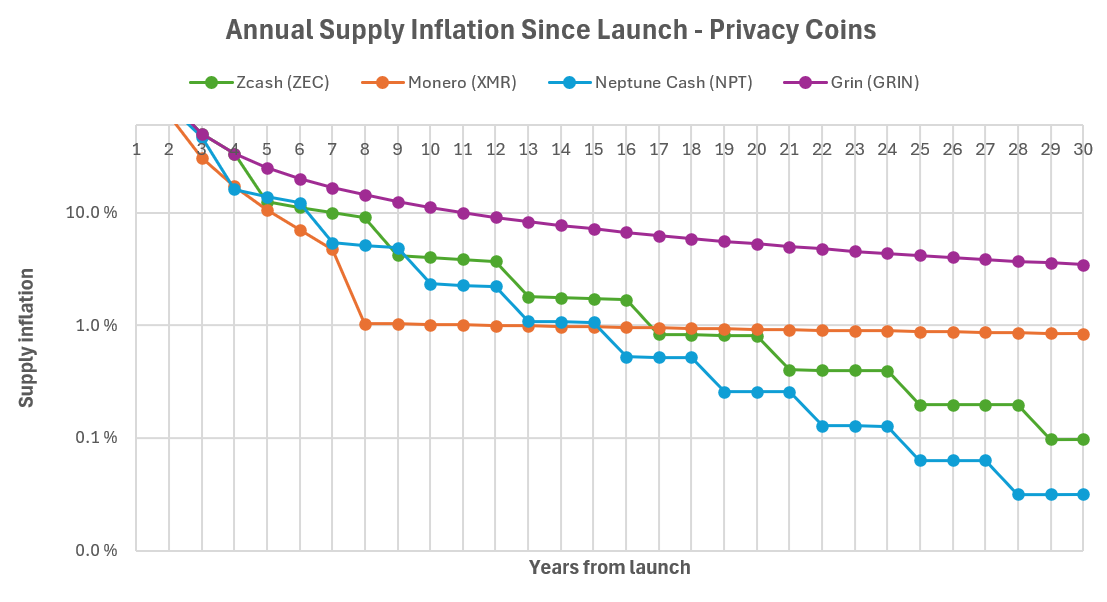

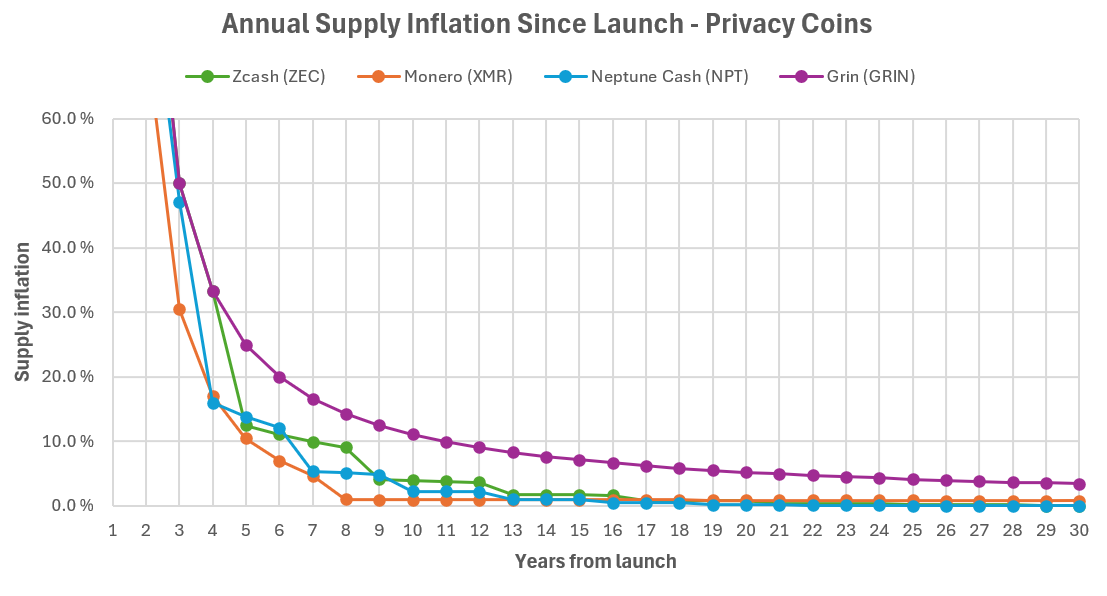

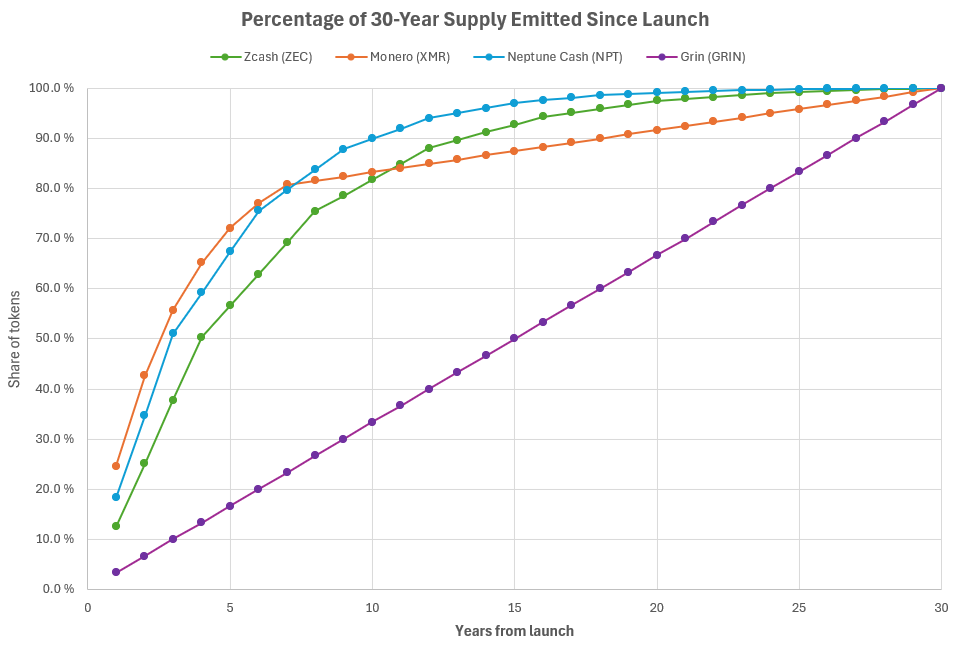

“OK, then. I guess increasing future emissions are bad but what about decreasing them? Can’t you slow down inflation, or reduce the total supply to create a price boost that will attract more retail investors and thus make the network more popular?” No. We cannot. First of all, it would violate the principle that the emission schedule is fixed. Secondly, it would be unfair to future stake holders and thus reduce the long-term potential of Neptune. To see why, take the extreme case where all the coins are minted in the first week. This setup would only allow very few people the opportunity to mine Neptune, and the network would forever be dominated by those early miners. If the emissions are instead distributed over decades, then many more miners have a fair chance to participate in the minting. That’s one of the reasons that emissions must be distributed over long time horizons.

The time to debate the emission schedule was prior to launch of main net on February 11 2025. Now that main net is launched that window has passed. After all, code is law.

It should be noted, though, that the author is of the opinion that a functional blockchain takes precedence over the emission schedule. After many halvings, decades from now, it might be the case that the incentive to mine is not sufficient to protect the network against double-spending attacks, since reorganizations become cheap due to the diminished incentive to mine. If that were to happen, it would be up to the community and to the market in the future to consider a change of the rules to allow for tail emissions, such that there always exists an incentive to mine. For the author, this would be the only acceptable argument for a change to the emission schedule: to keep the blockchain functional, not to attempt to manipulate a price.